Where the Numbers Come From

We take the current universe of 3000+ US-listed ETFs and filter for those that have been around for least 2 years, leaving ~2200 funds. This is consistent with the launch pace of ~400 funds per year in each of 2021 and 2022. We regress all funds’ 24+ month total-return data on the FF6 factors (FF5 + UMD). Based on those results, we impose the following additional filter criteria:

| Criteria |

Lower Bound |

Upper Bound |

| Implied Relative Factor Sharp |

1.0 |

N/A |

| Market Beta Coefficient |

0.8 |

1.2 |

| AUM |

$50M |

N/A |

| Fund Lifetime |

10 years |

N/A |

| Annualized Dividend Yield |

0.5% |

N/A |

Implied Relative Factor Sharpe is the ratio between the ex-post Sharpe ratio of a synthetic fund with factor loadings equal to those derived in the regression, including alpha (the regression intercept), divided by the market Sharpe ratio, both over the full period of Kenneth French’s factor data starting in July of 1963 (nearly 60 years of data). As expected, alpha is nearly always negative and equates to trading costs plus management fees. We submit that Relative Factor Sharpe is the ultimate acid test of fund viability; regardless of a fund’s performance over the analysis period, if it would not have generated a superior risk-adjusted return over the full history of factor data under ideal conditions, then it has no rational place in a portfolio.

Here’s a somewhat shocking-fact that speaks to the cost and inefficiency of implementing factors in long-only funds: when we filter our ~2200 fund analysis universe down to those that have a positive Relative Factor Sharpe, we are left with just 170 funds. Once we impose our 10 year lifetime restriction, the list drops to just 70 funds. 56% of all funds have statistically-significant (t-stat > 1.96) exposure to at least one of the FF6 factors, and can reasonably be identified as ‘smart-beta’. Of these, just 19% justify their existence, net of negative alpha (implied fees and transaction costs). That means 81% of all ‘smart-beta’ funds leave the investor worse off than a simple low-fee cap-weighted total-market passive fund like IVT. Surfacing the best of this short list of funds is the essential mandate of our efforts, here.

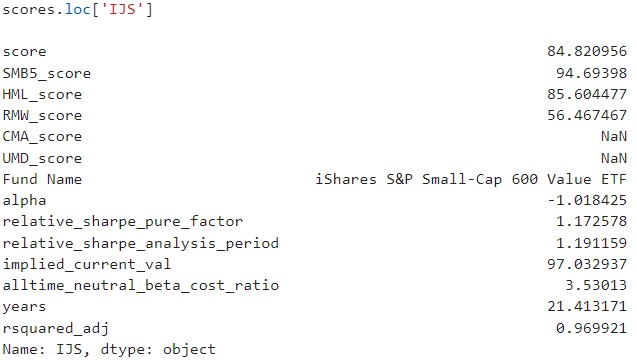

Back to IJS versus DFSVX: IJS earns an overall score of 85%. Mathematically, it has a Relative Factor Sharpe of 1.17 (17% better than the plain-vanilla market over the analysis period). See the figure below for further stats; Relative Factor Sharpe is identified as ‘relative_sharpe_pure_factor‘ in the analysis output. This means that IJS has a Relative Factor Sharpe equal to 85% of the 95th percentile fund in the analysis. In this case, the 95% percentile fund has a Relative Factor Sharpe of 1.38 (1.17 / 1.38 = 85%). (Several funds fall into the 95% percentile or better, and we’ll discuss other attractive candidates and their factor capture in future posts). At 91%, DFSVX has a Relative Factor Sharpe of 1.26, 26% percent better than the market, and 7.7% better than IJS, making DFSVX the superior choice on a risk-adjusted basis, ex-ante, if we take ex-post synthetic returns and factor capture as our best predictor of forward fund returns.

We also include two ‘Factor Waterfall Charts’ for direct comparison between the two funds’ factor return contributions over the ~21 year analysis period (charts are interactive, so feel free to zoom and pan). DFSVX picks up 20bps with a slightly-greater market beta (we could have volatility-normalized to equal market betas), 10bps in SMB, 20bps in HML, 40bps in RMW, -20bps in CMA, and a further 50bps in residual Alpha, for a total of ~70bps of outperformance. DFSVX is 7% more volatile than IJS over the analysis period, and delivers almost exactly 7% greater absolute performance (this margin is larger if we use returns in excess of the risk-free rate); Sharpe ratios are therefore similar over the analysis period. DFSVX comes out on top because of its historical factor mix which drives the superior Relative Factor Sharpe measure (see above).

For those interested, here’s a quick run down of the other key metrics in the analysis. The various factor scores in the bar charts, above, are their % of the value of the 95% percentile fund ranked separately on the individual factors. DFSVX’s score of 100 in HML, for example, means that its HML factor exposure is at least greater than the 95th percentile fund among those with statistically-significant HML exposure. ‘alpha‘ is the annualized fund implementation cost, ‘implied_current_val‘ is the ratio between the current dividend yield, and the average historical dividend yield (stated in %) as a somewhat crude proxy for current valuation, and ‘alltime_neutral_beta_cost_ratio‘ is the ratio of implementation costs to the expected smart factor beta, net of market beta. In other words, it’s the return on implementation drag; IJS has a 3.5X ratio, which means that for every 100bps of fees and implementation costs, 350bps of expected smart factor beta is delivered in return; clearly the bigger the better, with ratios under 1.0 defining a fund that is not justifying its existence (even without adjusting for volatility, as is accounted for with the Relative Factor Sharpe measure).

It’s natural to ask: which other Small Value funds rank in the 95th percentile with scores of 100 and are among the relatively few funds that justify their existence as smart beta? We’ll cover those in upcoming reviews.